|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

||

|

|

|

|

Understanding 20 Year Home Refinance Rates for Better Financial PlanningWhen considering refinancing your home, it's crucial to understand the nuances of different term lengths. A 20-year refinance offers a unique balance between the shorter 15-year and longer 30-year options, providing an opportunity to reduce interest costs while maintaining manageable monthly payments. Benefits of a 20-Year RefinanceChoosing a 20-year refinance can offer several advantages that might align well with your financial goals. Interest SavingsOne of the primary benefits is the potential for significant interest savings over the life of the loan compared to longer-term options. This can be especially appealing if you want to refinance to add onto house projects or other financial goals. Faster Home Equity BuildingA shorter term means more of your payment goes toward the principal, helping you build equity faster.

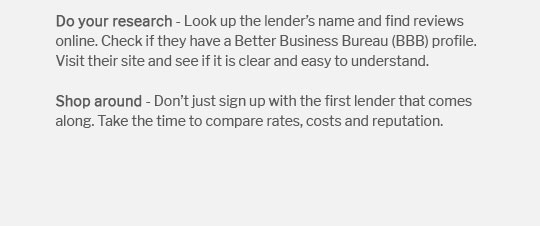

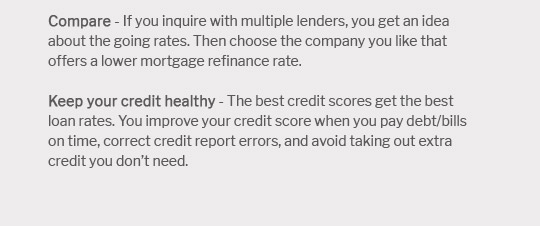

Considerations Before RefinancingWhile refinancing can be beneficial, there are important factors to consider before proceeding. Credit Score ImpactYour credit score plays a crucial role in determining your new interest rate. Homeowners with a refinance with 680 credit score may find competitive rates. Closing CostsRefinancing involves upfront costs, which can offset savings if not planned for appropriately.

Frequently Asked QuestionsWhat is the average interest rate for a 20-year refinance?Interest rates fluctuate based on market conditions and individual financial profiles, but they typically fall between 3% and 4% for a 20-year refinance. How does refinancing affect my monthly payments?While the interest rate and loan term impact monthly payments, a 20-year refinance generally results in higher payments than a 30-year loan but lower than a 15-year loan, striking a balance between affordability and savings. Is a 20-year refinance right for everyone?Not necessarily. It depends on individual financial situations, goals, and the ability to manage the monthly payments associated with a shorter loan term. https://www.bankrate.com/mortgages/20-year-mortgage-rates/

Weekly national mortgage interest rate trends ; 20 year fixed, 6.93% ; 10 year fixed, 6.33% ; 30 year fixed, 7.11% ... https://www.zillow.com/mortgage-rates/20-year-fixed/

and the annual percentage rate was 7.393 percent. on October 27th, 2024, the rate was 6.765 percent,, and the annual percentage rate was 7.413 percent. on ... https://money.usnews.com/loans/rates/mortgages/20-year

As of January 23, 2025, the average 20-year-fixed mortgage APR is 6.80%. Why Trust Us.

|

|---|